Freight rates drop, but energy crisis expected to keep commodity prices higher for longer

Market and business update - November 2022

Read report as PDF here

Read report as PDF here

The crude oil prices, freight rates, and transit times have downturned significantly over the recent months, but commodity prices are still riding high due to elevated energy prices. Also, adverse weather conditions in parts of the world and increased labor costs, within transport and logistics, add to pain. markets are still characterized by inflation and volatility. The crude oil prices, freight rates and congestion rates have downturned over the recent months, but still remain on a considerably higher level than before Covid and the Russia-Ukraine war. Also, extreme drought in different parts of the world, adds to the pain, especially in the grain and electricity markets. These disruptions cause ripple effects on the commodities, but still our delivery capacity remains very strong.

This market and business update intends to give you an indication of the expected price development of the most important commodities, freight rates, supply chain challenges, the additional effects of labor shortages, and challenges in major ports.

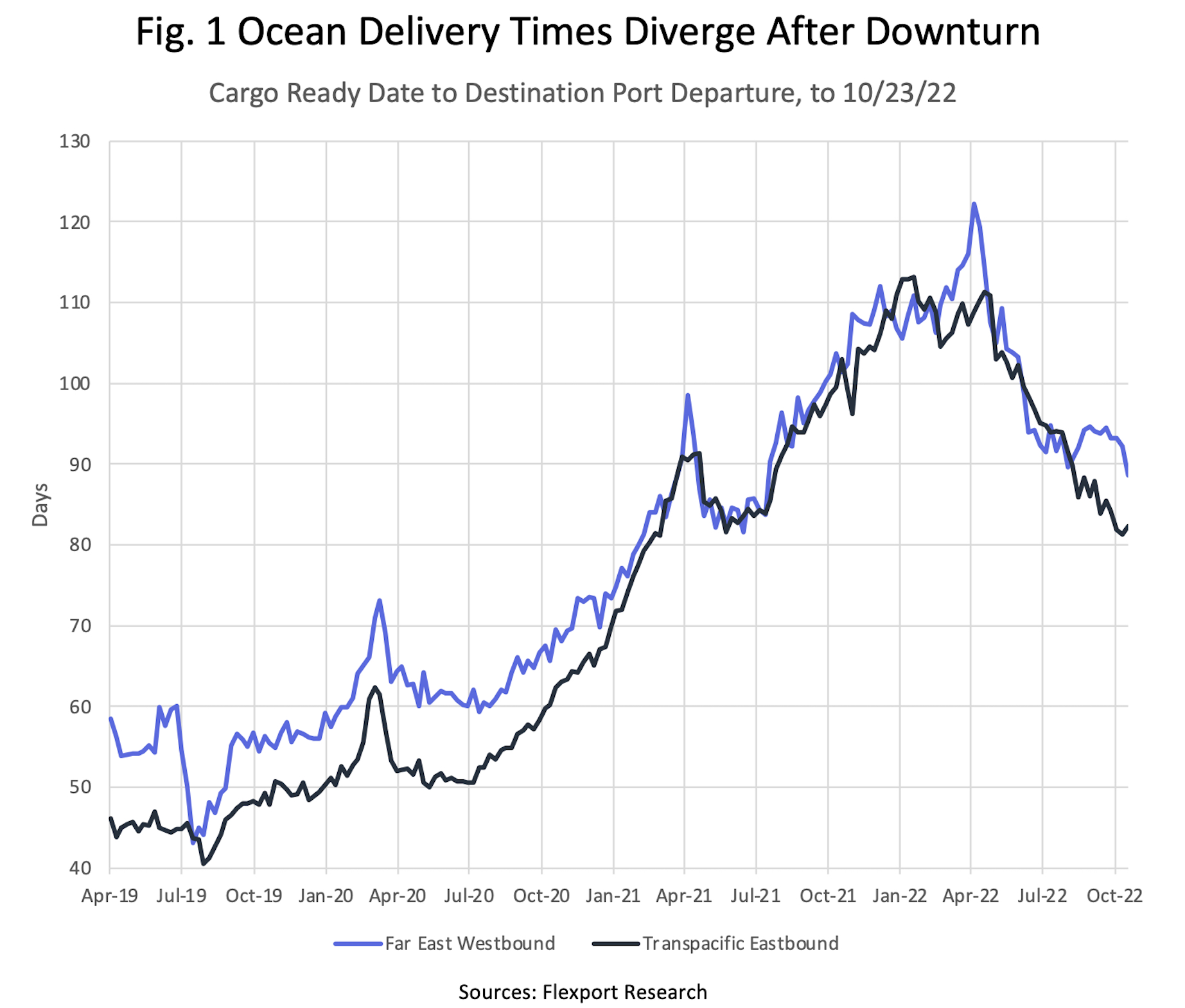

Continuous downturn in transit times

TPEB and FEWB transit times fell even further in October, compared to September 2022. According to the Flexport Ocean Timeliness Indicator, the continuous downturn is clear, though transit times still remain above pre-pandemic levels. TPEB fell to 82 days, and FEWB dropped to 89 days. The continuous downturn comes before the peak season, and we might see new bottlenecks and increasing wait times in the coming months.

The Flexport Ocean Timeliness Indicator (OTI)

Transpacific Eastbound (TPEB)

- October 2019: 48 days

- October 2020: 60 days

- October 2021: 102 days

- October 2022: 82 days

Far East Westbound (FEWB)

- October 2019: 57 days

- October 2020: 67 days

- October 2021: 103 days

- October 2022: 89 days

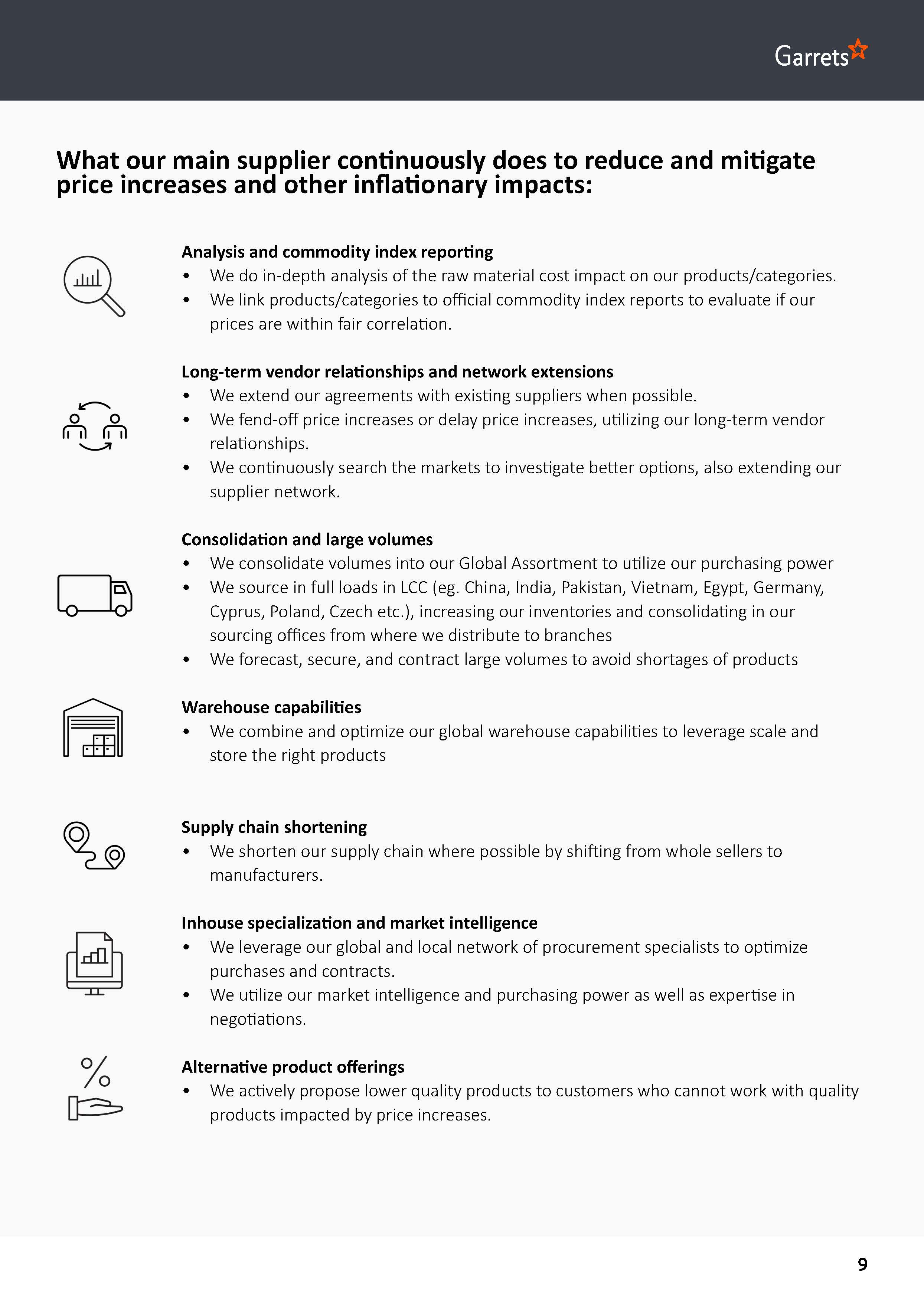

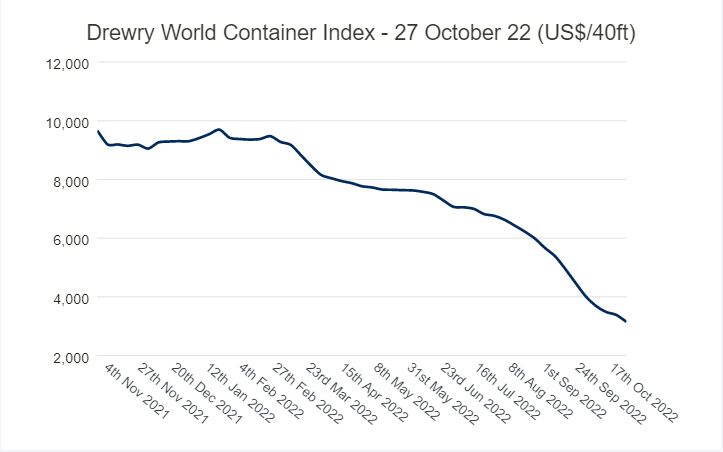

Freight rates now 70% below peak reached in September 2021

According to the Drewry World Container Index, a 40-feet container has dropped 70% since its peak in September 2021, indicating a return to more normal price levels. However, the container index still remains 121% higher than average pre-pandemic rates in 2019. Looking into 2023, freight rates are estimated to further drop due to a decline in consumer demand and a wave of new vessels hitting the water (Source: Freightwaves). The arrows are already pointing down. Capacity is being removed by slow steaming, and in September, we saw low imports to Long Beach and Los Angeles despite the fact that September is traditionally a high-volume month for end-of-year products (Source: Freightwaves).

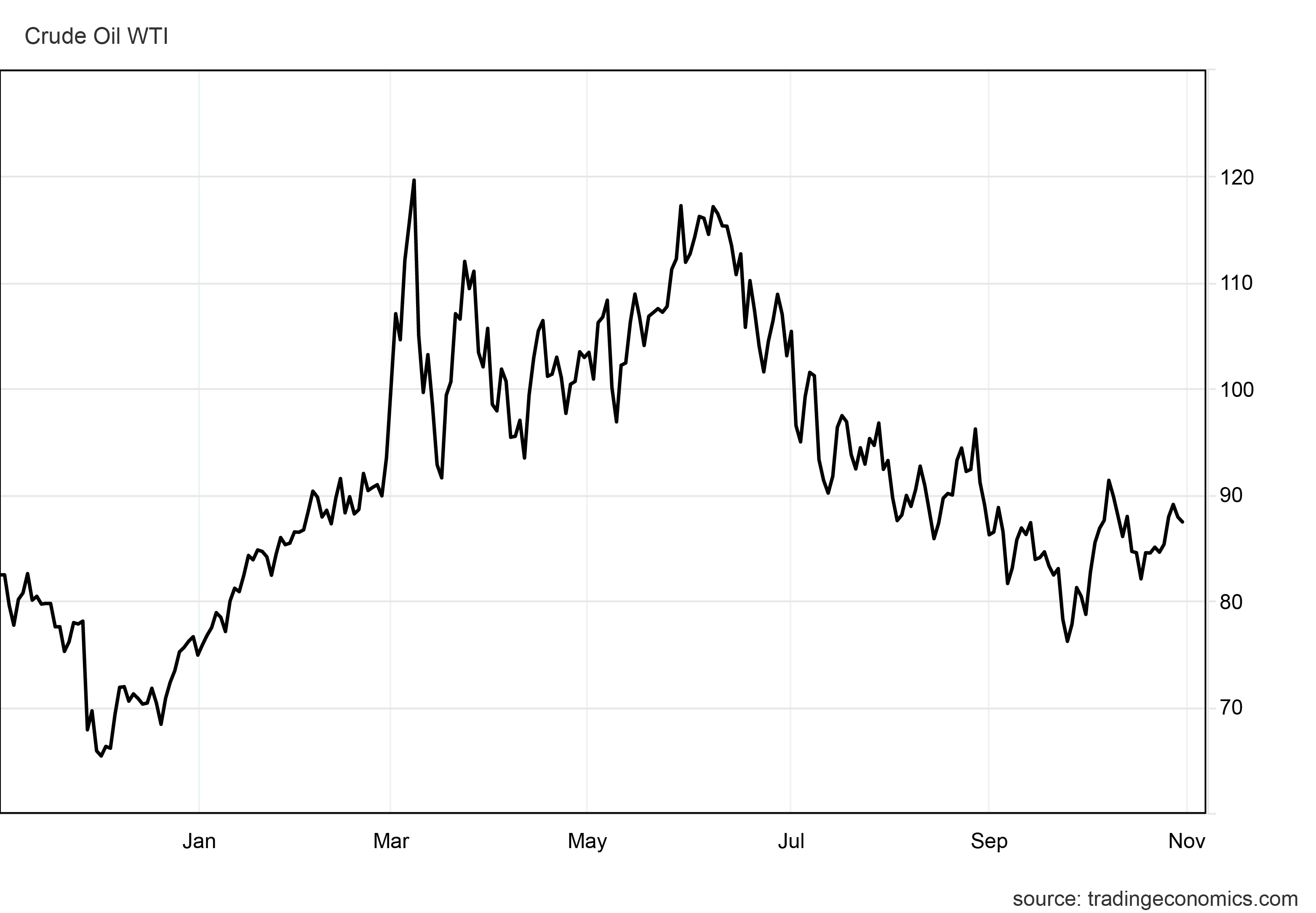

Oil prices dropped for the fourth month in a row, but estimated to increase next 12 months

Driven by expectations of an economic slowdown, the crude oil prices saw the fourth consecutive monthly decline, reaching its lowest pre-pandemic level in September at around USD 76 per barrel. Still, oil prices increased to around USD 88 in October after OPEC-countries agreed to cut production in November. In 12 months’ time, oil prices are estimated to be traded at around USD 99.87 due to these tighter global supplies.

Source: Trading Economics Index.

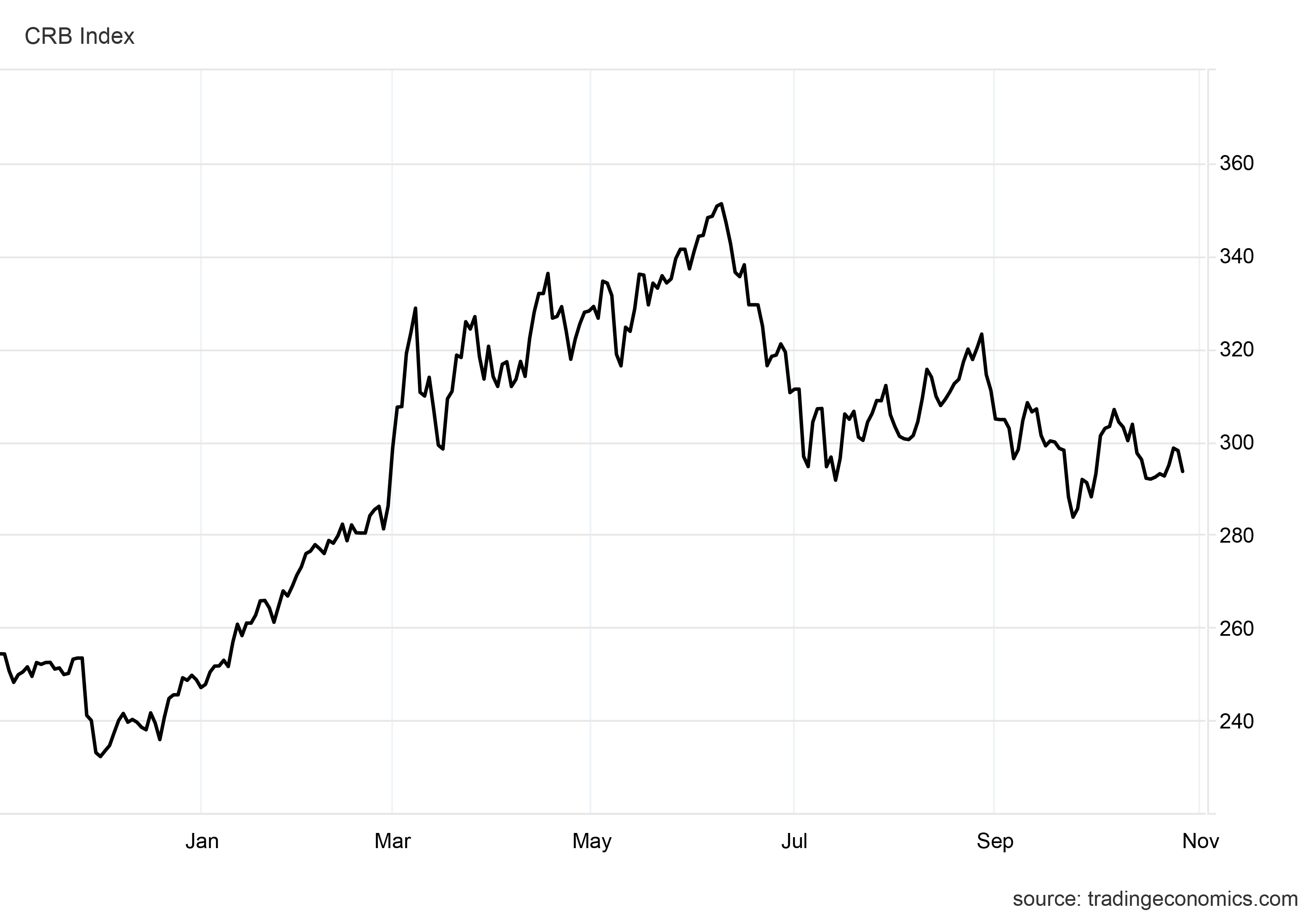

Inflationary impact on commodities, up 19% since beginning of 2022

According to the CRB Index, the commodity prices increased by 46.57 points or 19% since the beginning of 2022, elevating also the price level of certain provisions and stores. However, due to the intermediate downturn of the commodity index from July to October this year, some provisions and stores have stabilized or decreased slightly. In 12 months time, commodities are estimated to increase by around 7% as energy prices are expected to remain well above pre-pandemic level. As recently as 29 October, Russia suspended the United Nations-brokered deal to secure the export of Ukrainian grain out through the Black Sea. The suspension is expected to impact global food prices directly, especially for wheat.

Energy prices, adverse weather patterns and labor costs - part of the inflationary impact

The industry is finally getting some relief with direct supply chain costs. Freight rates, oil prices and transit times have dropped during the recent months, though still at a significantly higher level than before Covid 19. But several other factors including sky-high energy prices, adverse weather patterns and labor costs have maintained the high commodity price level.

Energy prices

Energy prices including oil, natural gas and coal prices reached an all-time high earlier this year, impacting production costs including heating, electricity and manufacturing. Further, the global spare production capacity buffers in 2022 have declined. Even though energy prices have declined from record highs earlier in 2022 and are expected to decline further over the next two years, they will still remain well above their recent five-years average (Source: The Worldbank Commodity Markets Outlook, October 2022).

Adverse weather patterns

Adverse weather patterns have also impacted the world food price level. At a global level, maize production is expected to decline 4% this season, in response to weather-related lower yields in the United States and the EU. Global rice production is expected to decline by 5% reflecting, among others, lower crops in China due to dry conditions (Source: The Worldbank Commodity Markets Outlook, October 2022) and flooding bringing destruction to rice crops in Pakistan (Source: Gro Intelligence).

Labor costs

The shortage of labor capacity and the need for additional capacity to meet the increasing demand during and after Covid, has impacted the salary level of transport and logistics significantly. According to FreightWaves, some American transport companies have raised driver pays by 10-12% since the pandemic started. In The Netherlands, they are negotiating collective labor agreements for transport and logistics with trade unions of around 7.5% for 2023. The lack of labor capacity across many sectors, including transports and logistics, is part of the catalyst driving inflation, and part of the reason why commodity prices remain high.

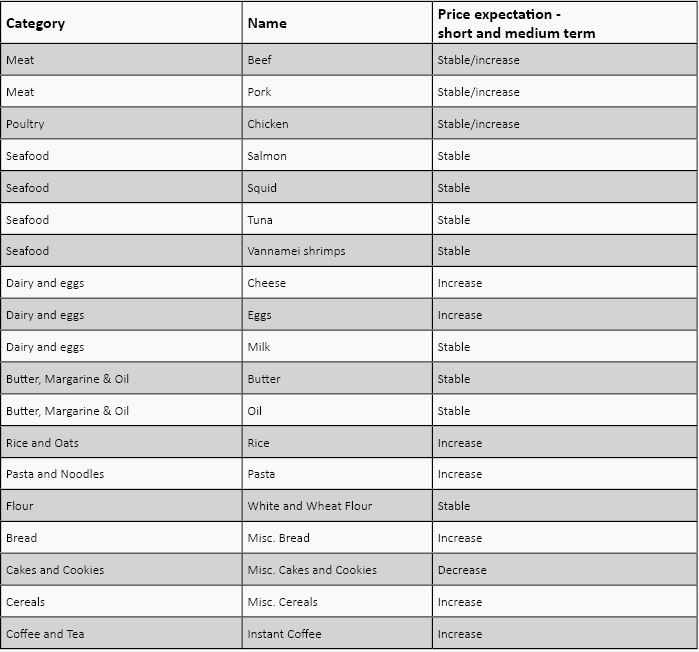

Inflationary impact on provisions on short and medium term

On short term, we do not foresee any major shortages on provisions as our existing contracts are still honored by our suppliers, giving high priority to large customers. However, this situation might change any time due to volatility, forcing us to substitute certain products with comparable products.

According to the FAO Food Price Index, food prices averaged 136.3 points in September 2022, down 1.5 points or 1.1% from August 2022, marking the sixth consecutive monthly decline. Still, food prices remained 7.2 points or 5.5% above its value compared to August 2021. Due to the inflationary effects, we expect certain price increases within the provision categories on short term. The list is not exhaustive.

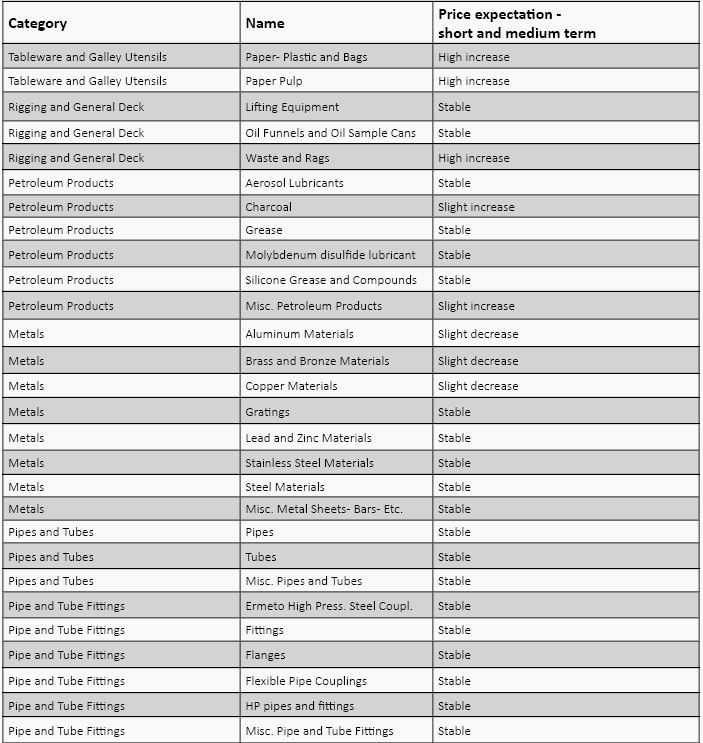

Inflationary impact on stores on short and medium term

On short and medium term, we do not foresee any shortages on technical consumables and stores. However, this situation might change any time due to volatility.

The raw material of several commodities is decreasing, but the increase in oil and gas prices in 2022 is feeding through into higher inflation, effecting raw materials, transport costs, energy costs and production costs. Due to the inflationary effects, we expect the prices of the following stores categories to increase on short term. The list is not exhaustive.

Inflationary and other macro impacts on major ports

| HOUSTON |

-

Freight rates: Domestic freight rates have somewhat stabilized, but they are still considerably higher than they were pre-COVID-19. Airfreight continues to have delays due to lack of labor, equipment, and airlines overbooking cargo, bumping cargo as needed to maximize space and profitability for the airlines. The struggles in the workforce, in this sector, have also caused cargo centers to reduce their hours of operation, especially in the evenings and weekends. These operational difficulties and changes have definitely had an impact on Spares/Owners’ Goods.

-

Backlogs: The Port of Houston and container freight stations have cleared the three to four week backlog that we previously were seeing; however, we are still seeing delays at point of origin. There is a three to five day delay due to a continued chassis shortage in the local market. Container rates continue to decline out of China. Steamship lines continue to reserve the right to cancel voyages due to a variety of reasons. While the backlog has improved, there is still congestion and we continue to get charged a congestion fee on each container pulled from the Port of Houston.

-

Steel related items: All steel related items that have been on backorder from China have finally delivered. The vast majority of US vendors that were struggling to fulfill product demand have recovered and are delivering in full.

Bird influenza: Due to a previous outbreak of bird influenza, we continue to see price spikes on both poultry and egg items, with eggs being the hardest hit.

-

Terminals: Also in the Western US Gulf, we continue to see an increase in launch/barge prices and terminal delivery fees. Many of the terminals, where we have seen this in, are the more strict terminals with a myriad of restrictions. We continue to work with agents and customers to provide the most economical locations to take supplies.

-

Labor market: The labor market remains challenged, and wages continue to rise due to fierce competition in finding and retaining quality labor.

-

Fog season: The fog season is upon us in the Western US Gulf (October to March). When fog hits the region, it causes delays both inbound and outbound as well as vessel diversions. This can disrupt our inbound supply chain as well as our ability to deliver on time in full to our customers.

|

| NEW ORLEANS |

- Drought: The Mississippi river drought issue is only getting worse. Now at all-time record lows in Memphis area, and still around 2,000 barges that cannot make it to the grain terminals in our area. Result is that we are seeing bulk vessels being diverted and also very short notice if they finally berth at a terminal which seems counterintuitive. To learn more about the Mississippi drought, click here: Mississippi River Or A Desert? Photos Show Stunning Impact Of Record-Low Water Levels (forbes.com)

|

| LONG BEACH |

|

| NEW YORK/ NEW JERSEY |

- Congestion: Congestion in New York/New Jersey is generally slowing down. During the week of September 19, Marine Traffic monitored 12 container ships waiting off of the Port of New York and New Jersey for an average of 9 days. High levels of imports have recently triggered a heavy backlog at the Port of New York and New Jersey, but backlogs are also slowing down.

|

| JACKSONVILLE |

-

Procurement: Our Global Procurement teams continue to evaluate our internal purchasing cost to the key benchmarks in each category using the USDA and FDA indices. We are continuing to implement mitigation strategies in our Procurement process to reduce the net increase to customers.

-

Operating cost: We are experiencing an exponential increase in our operating cost due to the fuel, insurance and maintenance fees going up.

-

Labor market: The labor market continues to be the most challenging that we have seen. We continue to face driver shortages and we have been forced to increase wages by over $5 per hour just to retain the great talent we have. We continue to face warehouse associate shortage, and we have been forced to increase wages by $3 - $5 per hour just to retain the people we have. We still struggle to find people, and the hiring is still very difficult.

-

Port congestion: Congestion in the South East continues in certain ports (Savan-nah and Charleston the highest). Over 40 vessels currently sitting at anchorage outside of Savannah.

-

Steel prices: Steel prices continue to increase and we don’t see that changing anytime soon.

-

Potatoes: Potatoes have seen a 100% increase in price over the last 4 months. Want to learn more? Please read the article:

https://www.boisestatepublicradio.org/news/2022-08-09/idaho-potato-shortage-harvest-spud

-

Time of season: Prices have increased up to 30% based on availability and the vendor having to source from other areas in the US as well as foreign markets.

-

Airfreight: Airfreight is experiencing severe delays due to lack of labor and equipment which is impacting spares. Customers need to send spares well before the berthing schedule.

|

| MONTREAL |

-

Labor market: The labor market is extremely challenging right now. The Q3 results have not come out yet, but based on the article posted by statistics Canada, the job openings across Canada has reached nearly 1 million open positions, 997K to be exact. This is up by over 296,500 job openings to fill from Q2 of 2021.

-

This has caused issues for our suppliers not being able to fulfil orders because they simply “don’t have the staff”.

-

We had an example last week where our fresh supplier could not make a delivery as he did not have a driver, but we managed to replace the supplier.

-

Our competitors are also seeing staffing issues. Earlier this month, we almost had to take over a delivery since our competitor did not have any drivers to make the delivery.

-

Congestion: Port congestion has caused some berthing delays in Montreal and surrounding ports.

Fuel: Fuel costs are increasing again as fuel supply is beginning to be reduced.

|

| VANCOUVER |

-

Backlog: Westshore coal terminal recently concluded a 4-week strike, where the terminal halted work for the entire strike. This has caused some backlog that is quickly being resolved.

-

Avian flu: Due to avian flu, we have seen an increase in prices of eggs and chicken from the US as there are few states which are allowed to export to Canada.

-

Crops: Canadian grain and Canola crops for 2022 are set to rebound from last years’ drought which ravaged the crops.

|

| PORTLAND |

- Congestion: We expect increased port congestion and length of time ship will spend at anchor in Portland as grain ships are coming in, and rain has returned to the pacific northwest.

|

| SEATTLE |

- Congestion: To a minor degree, we expect increased port congestion and length of time ship will spend at anchor in Seattle as grain ships are coming in, and rain has returned to the pacific northwest.

|

| DUBAI |

-

Rice: Import issues of rice due to very strictly, newly imposed regulations that result in less availability in the market and price increases.

-

Flour: India has issued an export ban of ATTA flour. No Indian origin is available which is boosting price level of other origins.

-

Turkeys: Severe bird flu among turkeys has limited the availability and approved exporters of turkeys. Due to high demand for Thanksgiving and upcoming Christmas, prices are increasing significantly.

|

| SINGAPORE |

-

Eggs: Prices for eggs remain high and are also increasing slightly due to Malaysia protecting local prices and availability. Singapore’s own production is still low and imported eggs from Poland/Ukraine are still with limited availability.

-

Vegetables: Monsoon season in Malaysia puts pressure on especially green and leafy vegetables when it comes to quality and price.

|

| ROTTERDAM |

- Labor shortage: Labor shortage still continues to disrupt supply chains. In the Netherlands, we are negotiating collective labor agreements for transport and logistics with trade unions. If the unions agree, it will mean a salary increase of at least 7.5% for 2023 and a one-time fee of EUR 250 in January 2023. Together with the increasing fuel costs, this will have a significant impact on logistics costs.

|

| ALGECIRAS |

- Stock compliance: From time to time, we face problems to comply 100% as some items are not available anywhere due to lack of raw material. The stock outs last a few days.

|

| AALBORG |

-

Provision prices: Price level for certain provisions is still getting higher.

-

Shortage: Shortage of commodities in specific categories effects other commodities as demands move from one commodity to another, but apart from occasional shortages, business is returning to a more stabilized level.

|