Keep up-to-date with the latest Garrets news.

12 March 2026

How Nutrition Data Turned Into Action Improves Crew Health and Retention

When declining crew health and retention was linked to on-board diet, a global shipping company required insight to protect operational stability. By transforming vessel stock data into nutritional intelligence, Garrets enabled targeted performance optimisation with clear operational impact....

06 March 2026

Give to Gain: Contribution and Progress Across Garrets

International Women’s Day invites reflection on contribution and progress, both individually and as an organisation – a cause I fully support....

03 February 2026

The Crew-Centric Approach to Strategic Provisioning

Seafarers operate in demanding conditions where health, alertness, and morale are critical to safety and performance. In this environment, food is far more than sustenance....

20 January 2026

Provision Strategy and Crew Retention - A Cost Multiplier

Crew turnover is one of the most expensive and persistent challenges in the maritime industry. Yet one of the most influential drivers of crew retention is frequently overlooked: On-board food....

17 December 2025

The Business Case for Responsible Cost-Effective Provisioning

For maritime executives balancing budget discipline with sustainability commitments, responsible food provisioning is one of the most cost-efficient levers available....

10 December 2025

The Overlooked Role of Provisions in Shipping Responsibility

Food provisioning on commercial vessels is often treated as an operational necessity rather than a strategic lever. Yet, the quality and management of on-board provisions have a direct impact on two of the industry’s most pressing concerns: climate responsibility and operational cost efficiency....

30 September 2025

Garrets Leads the Way in Driving Food Sustainability at Sea

Supporting maritime businesses in shaping a responsible future for on-board food management to meet climate goals and improve crew wellbeing....

20 August 2025

What to Consider When Buying Provisions for Your Fleet

Ensuring that your fleet is well-stocked with quality food provisions is essential for maintaining crew health and operational efficiency. However, provisioning requires careful planning and attention to certain key factors....

17 June 2025

Investing in Culinary Development to Ensure Crew Wellbeing

Garrets enhances focus on improving the lives of vessel crew by expanding culinary development team to provide greater support to on-board cooks and stewards....

08 May 2025

The Hidden Costs of Poor Provision Planning - And How to Avoid Them

For many shipowners and operators, food provisions are seen as a simple cost and a necessary expense to keep the crew fed and operational. But poor planning in food provisioning does not just affect your budget. It can lead to hidden costs that impact efficiency, compliance and crew morale....

07 March 2025

Leading Women in our Business Driving Change and Growth

To mark and celebrate International Women’s Day (IWD) and its theme, Accelerate Action, Garrets International spotlights some of the remarkable women leading excellence in our global business....

21 January 2025

Expanding Our Footprint in Training Services to Support Crew Wellbeing

Crew wellbeing is a vital priority for the Garrets team. With responsibility for supplying safe food provisions to over 30,000 crew members globally, Garrets ensure positive outcomes on board through our specialised Cook and Galley Management training programs....

02 October 2024

Julian Baldey - New Business Development Director in Garrets

We are pleased to announce a significant update to our leadership team. As of October 2024, Julian Baldey will join us as our new Business Development Director....

17 September 2024

Mid-Autumn Festival: Harvest Season and Procurement Excellence

The Mid-Autumn Festival highlights the harvest season. At Garrets, we ensure vessels receive fresh, reliable provisions year-round by carefully aligning procurement with seasonal cycles....

05 September 2024

Join us at IMPA in London from 10-11 September – Booth #48...

24 July 2024

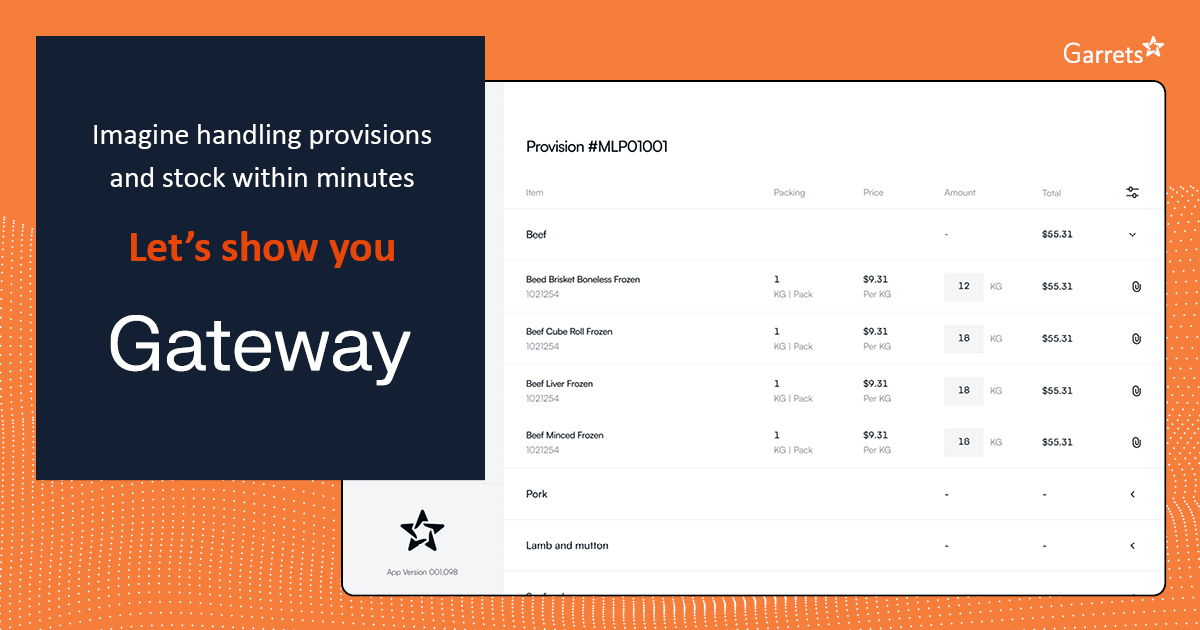

Imagine Handling Provisions and Stock Within Minutes

Streamline your operation with seamless provision management, budget oversight and effortless stocktaking...

25 June 2024

Celebrating Seafarers and Promoting Safety

Today, we join the global maritime community in celebrating Day of the Seafarer, a momentous occasion recognised by the United Nations and organised by the International Maritime Organisation (IMO)....

11 June 2024

Commitment to Genuine Partnerships at Sea

At Garrets, we believe that a better life at sea begins with the availability of fresh, high-quality provisions accessible at ports worldwide....

28 May 2024

Press Release - Wrist Posts Increased Growth and Continues its Major Digital Investments

As part of the Wrist organization, it’s a great pleasure to release the Annual Report for 2023....

24 May 2024

Market and Business Update - May 2024

The Red Sea crisis still prolongs the Far-East Westbound transit times due to the vessels rerouting via the Cape of Good Hope, driving up the global container price index....

16 May 2024

We are Excited to Meet You at Posidonia

Join us at Posidonia in Greece from 3-7 June – stand No. 3.411/1, Hall 3....

04 April 2024

Hamish Cook - New Managing Director in Garrets

We are pleased to announce that Hamish Cook has been appointed Managing Director of Garrets International as of April 2024....

05 February 2024

Market and Business Update - February 2024

Relatively stable commodity prices driven up by increasing freight rates...

24 January 2024

Safeguard the health care and safety of your crew with our medical supply and management service....

21 November 2023

Market and Business Update - November 2023

Elevated food price index stabilized since September, while some provisions still on the rise...

31 October 2023

Meet us at Crew Connect Global 2023 in Manila

Once again you can meet Garrets at Sofitel in Manila for one of the main crewing-focused events, Crew Connect Global....

13 September 2023

Market and Business Update - September 2023

Transit times and freight rates remained relatively stable in August and September, whereas crude oil prices have increased since June......

21 June 2023

At Garrets, we know that a better life is tied to health and responsibility. Therefore, we try to ensure that every crew has access to healthy, tasty, and nutritious meals by training and educating cooks – and by doing so turning cooks into heroes!...

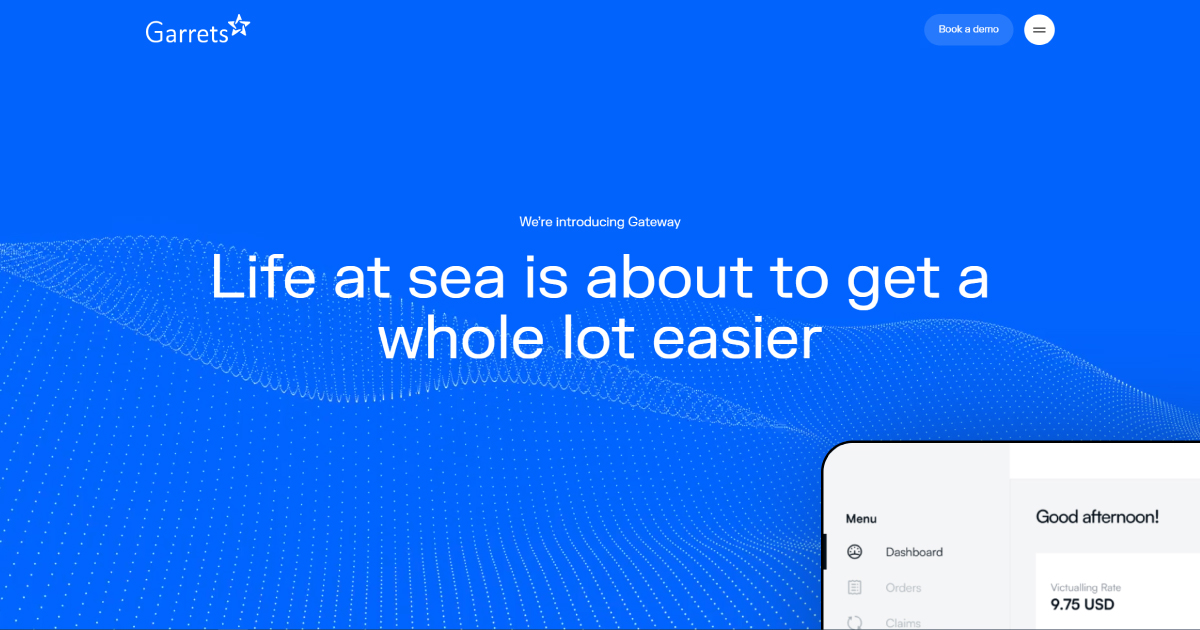

01 June 2023

Join Garrets in Oslo from 6-9 June. We will be ready at stand no. C01-38a to welcome you and show you how Gateway, our fast, easy and seamless ordering and stock management platform caters to your needs without compromise of convenience....

03 April 2023

Market and business update - April 2023

Commodity prices dropping marginally, but still remain highly elevated...

08 March 2023

International Women's Day - 8 March 2023

Today, we recognize International Women’s Day. It’s a day to celebrate the accomplishments of women within politics, business, society and digitalization, but it’s also the day to highlight the global work that remains to be done for gender equality...

23 February 2023

Garrets supports earthquake response efforts in Turkey and Syria

The consequences of the earthquake in Turkey and Syria are devastating. Our thoughts are with all the children and families affected by the terrible earthquakes in Turkey and Syria....

01 February 2023

Market and business update - February 2023

Energy prices and shortages in market supplies keep commodity prices elevated...

18 January 2023

Making life at sea better through careful and creative planning

– an insight in how we ensure a professional guidance on provision management for our customers...

08 December 2022

IMPA London is closing in! And we’re so excited – looking forward to welcoming new and existing customers to our booth for a talk about your provision and stores supply needs, budget management incl. our galley crew and cook training services....

02 December 2022

Fuelling better lives at sea with strong supplier network

This autumn, we have visited some of our key suppliers around the world to ensure safe, consistent and high-quality deliveries to our customers....

13 September 2022

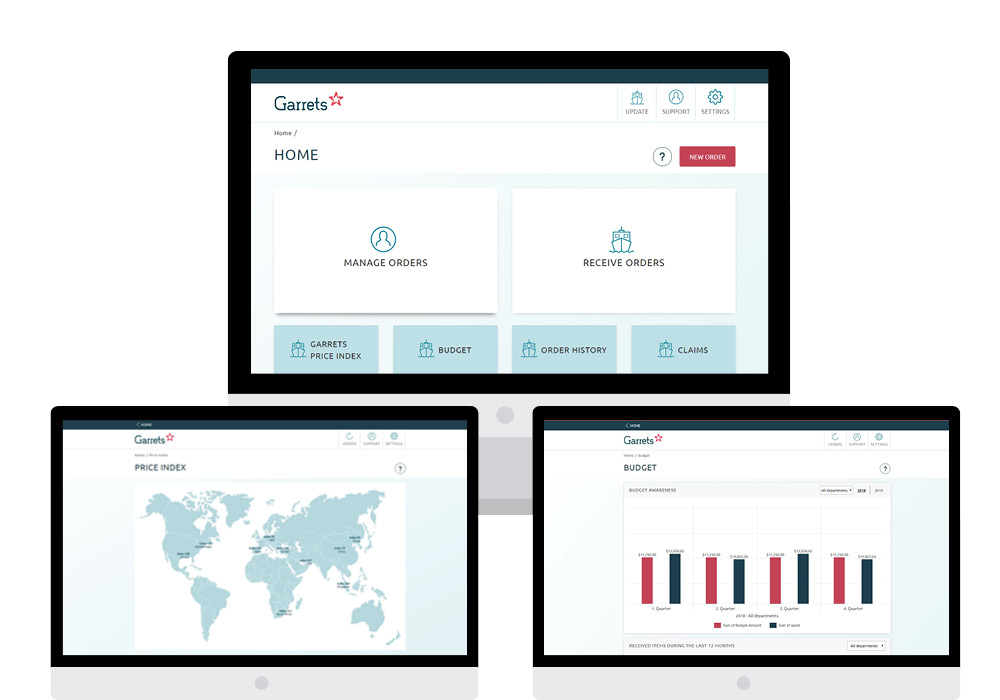

Gateway is the faster and smarter way of doing provision, stores and budget management on board. Start ordering faster, get price visibility, make smarter choices and manage your orders in one place....

09 June 2022

Through sponsorship and commitment, crucial healthcare comes alive on board Mercy Ships

Garrets has entered into a sponsorship agreement with Mercy Ships......

16 May 2022

MARKET AND BUSINESS UPDATE - MAY 2022

The shipping and ship supply industries are still characterized by uncertain market conditions and volatility....

30 March 2022

Inflationary impact expected to continue

The head winds of COVID-19 and the Russian invasion of Ukraine have a radical inflationary impact on commodity prices and general market conditions......

17 January 2022

Announcement - Lars Bomholt appointed Managing Director in Garrets

We are very pleased to formally announce that as from 1st January 2022, Lars Bomholt has been appointed Managing Director of Garrets....

30 September 2021

New preferred vendor, boosting our services in India

Following a rigorous evaluation process, we have awarded preferred vendor status for the next six months to a long standing supplier partner in India...

22 September 2021

ISO 9001 audit passed with flying colours

We are proud to inform that our UK office recently passed the ISO 9001 audit with no non-conformities or...

02 July 2020

Pre-Boarding Briefing Seminars carried out online

Our seminars shift to online sessions as we continue to serve our crews during COVID-19 times......

05 May 2020

Living through a global pandemic, most of us experience an atmosphere of fear, anxiety or uncertainty......

28 February 2020

A new month of vessel audits has passed and we would like to take this opportunity to present and recognise an impressive lineup of vessel crews, who have shown great passion and dedication in keeping their vessel crew going at sea....

25 February 2020

APM and Sea Japan exhibitions postponed

APM and Sea Japan shows have been postponed by organisers due to......

14 February 2020

It is hard to disagree that manufacturers should consider the impact on the environment and make it a priority......

01 January 2020

Our superintendents have spent the month visiting many impressive vessels and we would like to take this opportunity to recognise and appreciate the hard work and dedication that goes into keeping a vessel crew going at sea...

08 November 2019

Garrets offers digital tool for easy ordering at sea

The administrative burden when ordering goods is a challenge for many vessels....

16 October 2019

Garrets and Sailors' Society scholarship beneficiary graduates

In July 2018, Kristina Kamatoy from Quezon, the Philippines, began her training at the Magsaysay Institute for Hospitality and Culinary Arts (MIHCA) in Manila. Kristina is the second beneficiary of the maritime education scholarship funded by Garrets alongside the Sailor’s Society....

18 September 2019

International Seafarers Welfare Award 2019

As part of Garrets’ continual commitment to worthwhile charitable causes to benefit all seafarers Garrets Head of Commercial in the UK Rob Austin and Garrets Key Account Manager Mark Buckland-Garnett, representing both Wrist Ship Supply and Garrets, proudly presented two prestigious ISWAN awards on the 11th of September 2019....

16 August 2019

We welcome you at our stand at IMPA London from 10 - 11 September at QEII Centre, Westminster London....

03 June 2019

Introducing our new Executive at Garrets

We are pleased to announce that Stanley Morrice has been appointed Executive Chairman of Garrets International, effective from 1st of June....

10 May 2019

Meet us at Bari-Ship 2019 in Japan

We welcome you at our stand no. DEN-04 at the Danish Pavilion....

29 March 2019

Nominations - International Seafarers Welfare Awards 2019

Garrets recognises the excellent work of ISWAN to improve seafarers' welfare....

15 November 2018

Last week Garrets attended Crew Connect in Manila with great success....

05 November 2018

We welcome you at our stand at Crew Connect from 6 November - 7 November at Sofitel Philippine Plaza Manila....

02 August 2018

Update on scholarship funded by Garrets International

Our Superintendent Jerry Steele, had the great pleasure to meet up with Kristina Kamatoy...

26 April 2018

Welfare work for Seafarers recognized

Garrets international sponsors "Shipping company of the year" award....

16 April 2018

Introducing Garrets International in Japan

For the first time, Garrets took part in Sea Japan, at Tokyo Big Sight Exhibition Center....

19 March 2018

Thank you to all who visited us at APM 2018

Wrist and Garrets had a successful exhibition at last week’s maritime event....

15 March 2018

Press release: Wrist continued growing in 2017 - even in difficult markets

During 2017 Wrist Ship Supply kept working with customers......

08 February 2018

Meet us at Asia Pacific Maritime

Once again, Garrets will attend Asia Pacific Maritime (APM) in Singapore....

30 January 2018

The International Seafarers' Welfare Awards 2018

Garrets is proud to announce that we once again will be sponsoring Shipping Company of the Year award....

31 October 2017

Crew Connect is a global event for the crewing industry – “your crews, your conference”....

24 October 2017

Garrets sponsors Shipping Company of the Year award

For the 7th year, the International Seafarers' Welfare Awards recognise excellence in seafarers' welfare......

05 October 2017

Garrets is having a huge impact on the education of Edward!

In April this year we could tell the good news of supporting 22-year old Edward Cunanan by the help of Sailors Society....

21 September 2017

A successfully completed IMPA London 2017

We thank all visitors for stopping by at this years IMPA! We look forward to seeing you again next year....

04 August 2017

We welcome you at our stand at IMPA London from 12 September - 13 September at QEII Centre, Westminster London....

19 June 2017

Wrist and Garrets celebrate Day of the Seafarer

Together Wrist Ship Supply and Garrets International mark the annual Day of the Seafarer on 25 June....

07 June 2017

Thank you to all our visitors at Nor-Shipping 2017

Last week’s exhibition at the leading maritime event was a success for Wrist and Garrets...

08 May 2017

Garrets International, once again participates at Nor-Shipping 2017 in Oslo, Norway. Meet us at stand T01-15-A....

09 March 2017

Wrist saw growing market share in 2016

Sales increased by 13%. Despite tough market conditions – not least in the off-shore sector – Wrist Ship Supply continues developing its business platform....

27 January 2017

Garrets is now ready with dates for our Training Courses 2017!...

03 January 2017

How can we help seafarers to have focus on a healthy lifestyle?

Meet Garrets at this year's Wellness at Sea Conference 17 January 2017....

07 November 2016

This year’s Crew Connect in Manila takes place in November 2016. Garrets International is one of the leadership sponsors....

28 October 2016

The International Seafarers Welfare and Assistance Network (ISWAN) is holding a seminar on seafarers health....

05 October 2016

We aim to train the next generation of cooks!

Once again, we held a successful Cooks Training Programme in Nantong....

12 August 2016

Wrist and Garrets invite you to join us at SMM in Hamburg from 6-9 September 2016...

12 July 2016

Once again Garrets attends at MSSM in Nyborg in Denmark...

27 June 2016

International Seafarers Welfare Award 2016

The sixth year of the International Seafarers' Welfare Awards was held this Friday....

24 June 2016

Remember to celebrate our seafarers around the world...

17 June 2016

Training the next generation of cooks

We have just finished a two-day training seminar for a customer in Manila...

09 May 2016

Meet us at IMPA Singapore 2016

Garrets and Wrist Ship Supply will attend IMPA Singapore...

28 January 2016

Wrist Ship Supply today completed the acquisition of Garrets International Ltd....